We’ve written a VoxEU column for our patent paper, which you can find here.

Overview statistics

When I started writing this article I became curious how a typical VoxEU column looks like. So I scraped the archives and looked at some statistics. Here they are (as of November 15 2017):

After some cleaning, there are 5633 columns from January 2008 to November 2017.

The mean number of page reads of columns is 20,600 (median: 16,600).

The mean number of authors is 2.1 (median: 2). There are about 1800 single-authored columns.

The teaser text at the top of the columns contained 68 words on average (median: 66).

The main part of the column is a little harder to count, because it also contains tables, figure captions and references. When I just count all words before the first appearance of “References” in the text, I get a mean of 1383 words (median: 1327). That seems well within the recommended range of 1000-1500 words.

The most prolific writers have written up to 50 columns and the mean number of columns per author is 2.2 (median: 1).

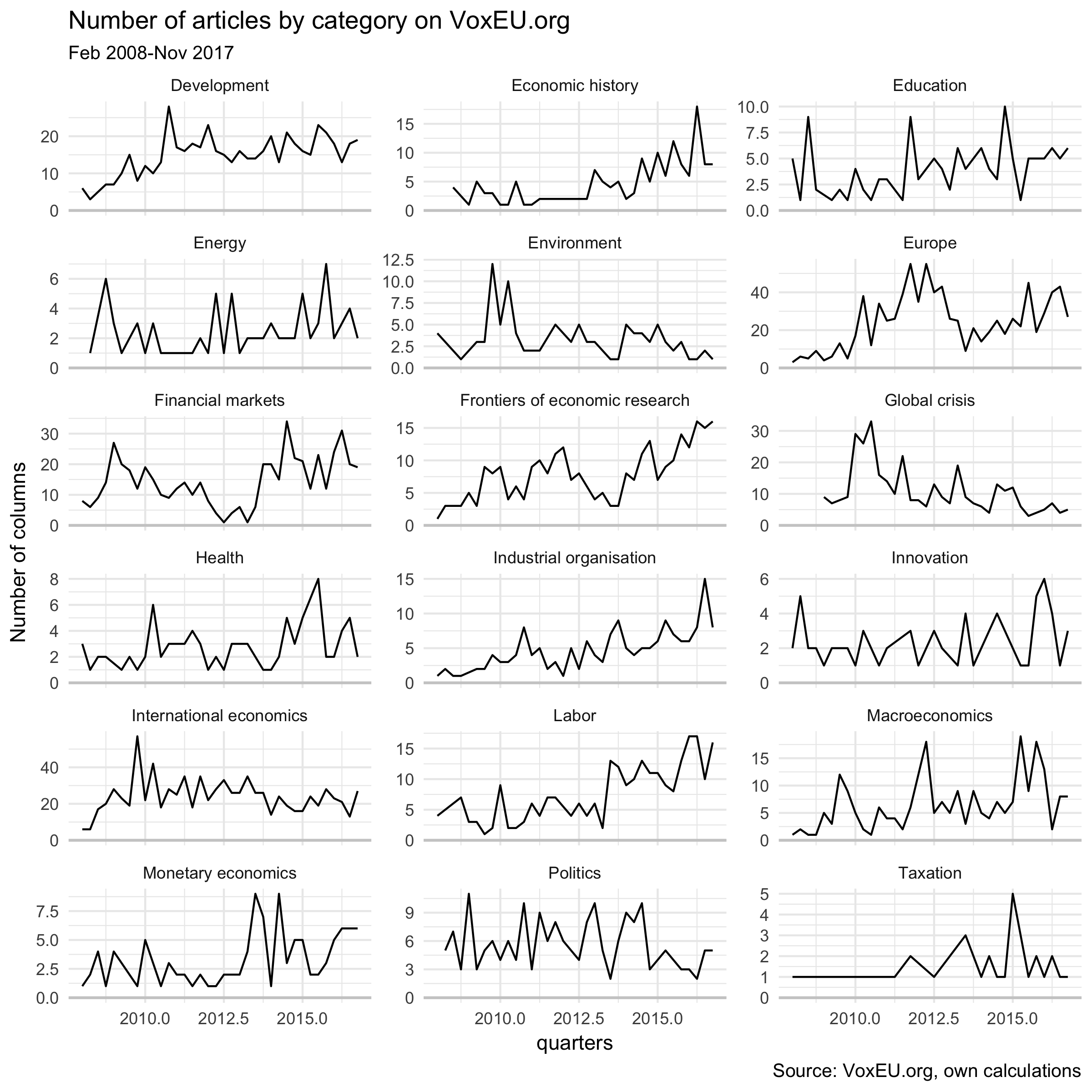

Every column is assigned to one topic and several tags. I aggregated the 49 topics to one of 19 categories (e.g., I counted “EU institutions” and “EU policies” as “Europe” and “Microeconomic regulation” and “Competition policy” as “Industrial organisation”). This produces the following figure:

Some observations:

The graph reflects the focus of voxeu.org. The top categories are “International economics” (950), “Europe” (930), “Development” (590), “Financial markets” (580).

Microeconomic theory and econometrics are only rarely covered.

The spike of the “Europe” category around 2012 might be related to the euro area sovereign debt crisis around that time.

The topic “Frontiers of economic research” is a bit more vague.

“Labor” and “Economic history” columns have become more important and columns with the topic “Global crisis” have become rarer.

Measuring complexity of text in columns

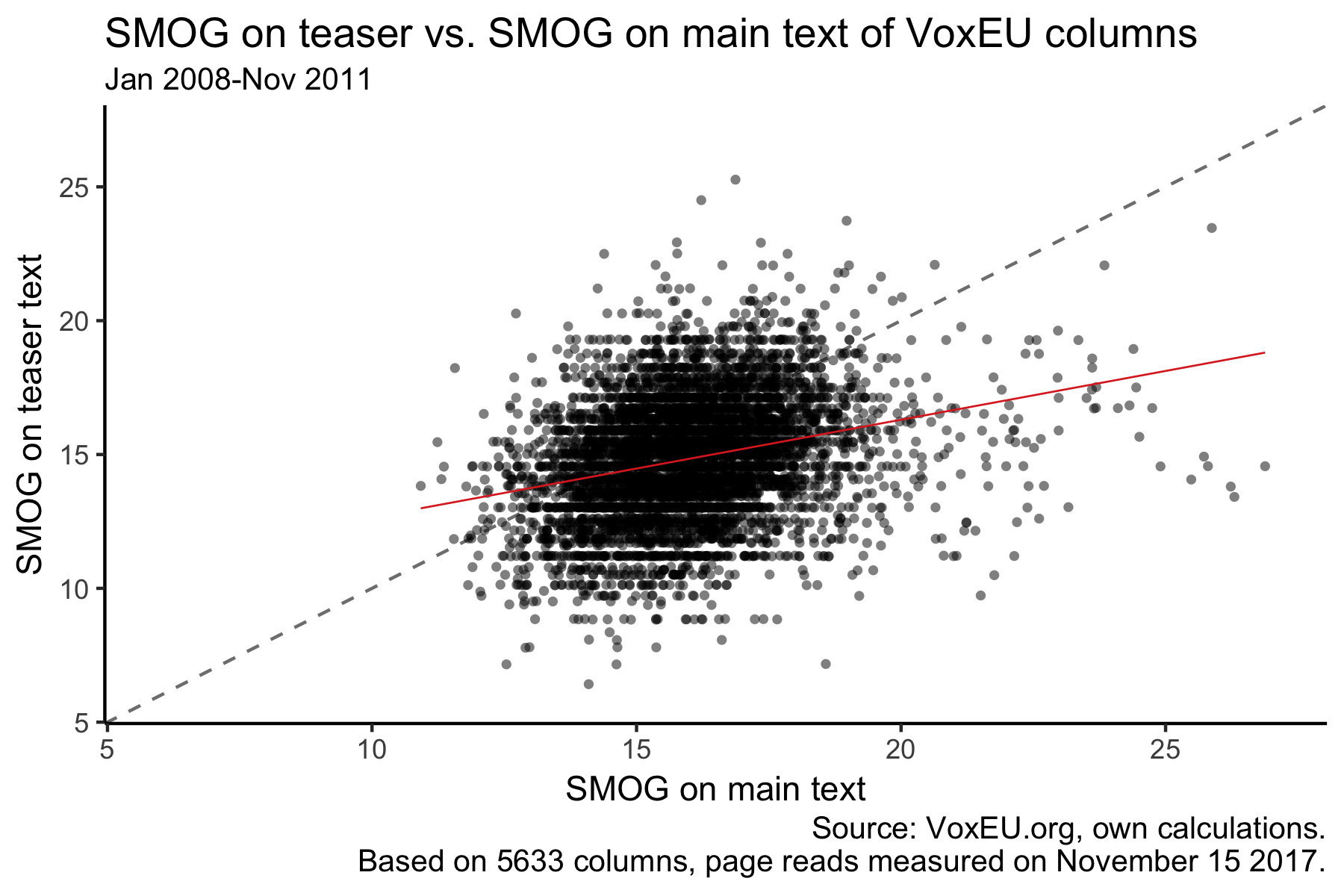

One fun exercise I’ve run is inspired by this blog post by Julia Silge. She explains how to use a “Simple Measure of Gobbledygook” (SMOG) by McLaughlin (1969) to find out which texts are hard to read. This works by counting the average length of syllables per words that people write. Words with fewer syllables are seen as easier to understand. The SMOG value is meant to show how many years of education somebody needs to understand a text.

I’m running this analysis separately on the columns teaser texts and their main body. Our own teaser text has 16 polysyllable words in four sentences and we calculate the SMOG value like this:

The rest of the column has 251 polysyllables in 65 sentences, which yields a SMOG of 14.4.

The winner of the VoxEU teaser text with the lowest SMOG count is this column by Jeffrey Frankel. It has a SMOG of 6.4, so taking the measure literally we would expect a kid fresh out of primary school to be able to understand it.

The column with the lowest SMOG value in its main column text is this column by James Andreoni and Laura Gee. It has 147 polysyllables spread out over 79 sentences, which yields a SMOG of 10.9.

I won’t name any offenders, but the highest SMOG score is 26.8. Understanding that text would require the substantial amount of education such as: 12 (school) + 3 (undergrad) + 1 (master) + 5 (PhD) + 6 (assistant professor) to understand.

The overall average SMOG value is 14.8 on teasers and 16.0 on main columns texts. So it seems that economists write on a level that college graduates can understand. SMOG doesn’t vary much by field, but it takes the highest value (on full columns) in “Industrial organisation” (16.9), “Monetary economics” (16.4) and lowest in “Economic History” (15.8) and “Global Crisis” (15.7).

The SMOG on the two column parts has a correlation of 0.27.

The OLS line is flatter than the 45 degree line which is probably a sign of the more accessible language in the teasers.

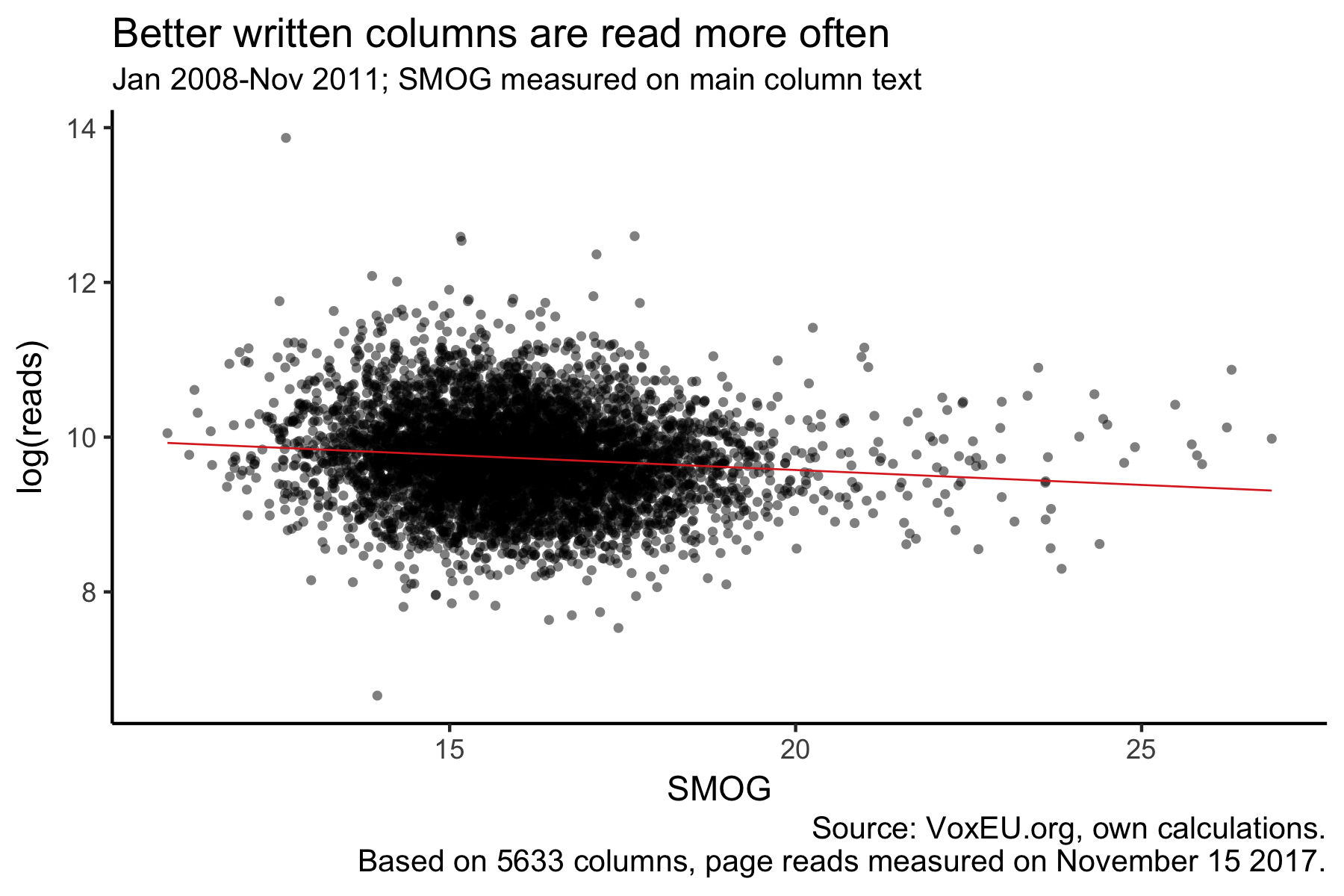

Interestingly, when we compare articles’ SMOG values with the number of times the page was read, we get the following negative relationship:

This also holds in a regression of log(page reads) on the SMOG values of both main text and teaser text, the number of authors, number of authors squared and dummies for the day of the week, quarter, year and – most importantly – the literature category (e.g. “Taxation”, “Financial markets” or “Innovation”). It’s not driven by outliers either and there is also a significantly negative relationship if I measure SMOG on the teasers only.

Writing columns that take an additional year of schooling to understand (SMOG + 1) is associated with 3 percent fewer page reads. Maybe that’s a reason to use fewer big words in our papers!

One explanation might be that more complex papers require the use of more big words. And that users on voxeu.org prefer clicking on articles that don’t sound too complicated. But better written papers might also just be inherently better in other dimensions. And because they’re more important, people read them more often.

References

McLaughlin, G. H. (1969). “SMOG Grading - a New Readability Formula”. Journal of Reading. 12(8): 639—646.

“Hitler’s Soldiers: The German Army in the Third Reich”, by Ben Shepherd. It find it hard to say I enjoyed this book, but it impressed me. Facts really stand out when Shepherd is able to put numbers on them. For example, did you know that, “During the winter of 1941-2, 360,000 Greeks died of famine”?

“Submission”, by Michel Houellebecq. What I found eerie is the psychological plausibility of the decisions in this story.

“Folding Beijing”, by Hao Jingfang. A fantastic (in both senses of the word) short story about reality and inequality by a Chinese macroeconomist.

“Hans Fallada: Die Biographie”, by Peter Walther (in German). I really enjoyed reading Fallada’s book “Alone in Berlin” and Fallada’s life was equally interesting. This superb biography spares nothing by simplifying too much.

“Commonwealth”, by Ann Patchett. We accompany the lives of six siblings over several decades. I started not expecting to finish, but after the first chapter I couldn’t stop.

“Gorbachev: His Life and Times”, by William Taubman. So much was new to me which mostly just reveils my ignorance about the topic.

At this point I know Jerome Powell only from news reports, though I was pleased to realize a few days ago that the locked-down Twitter account @jeromehpowell created in 2011 is following me, as well as several of my friends in the blogosphere. If he is reading this, let me say that I would be glad to craft a blog post on any topic he would like to hear my opinion on, and would be happy to do so while keeping his query confidential.

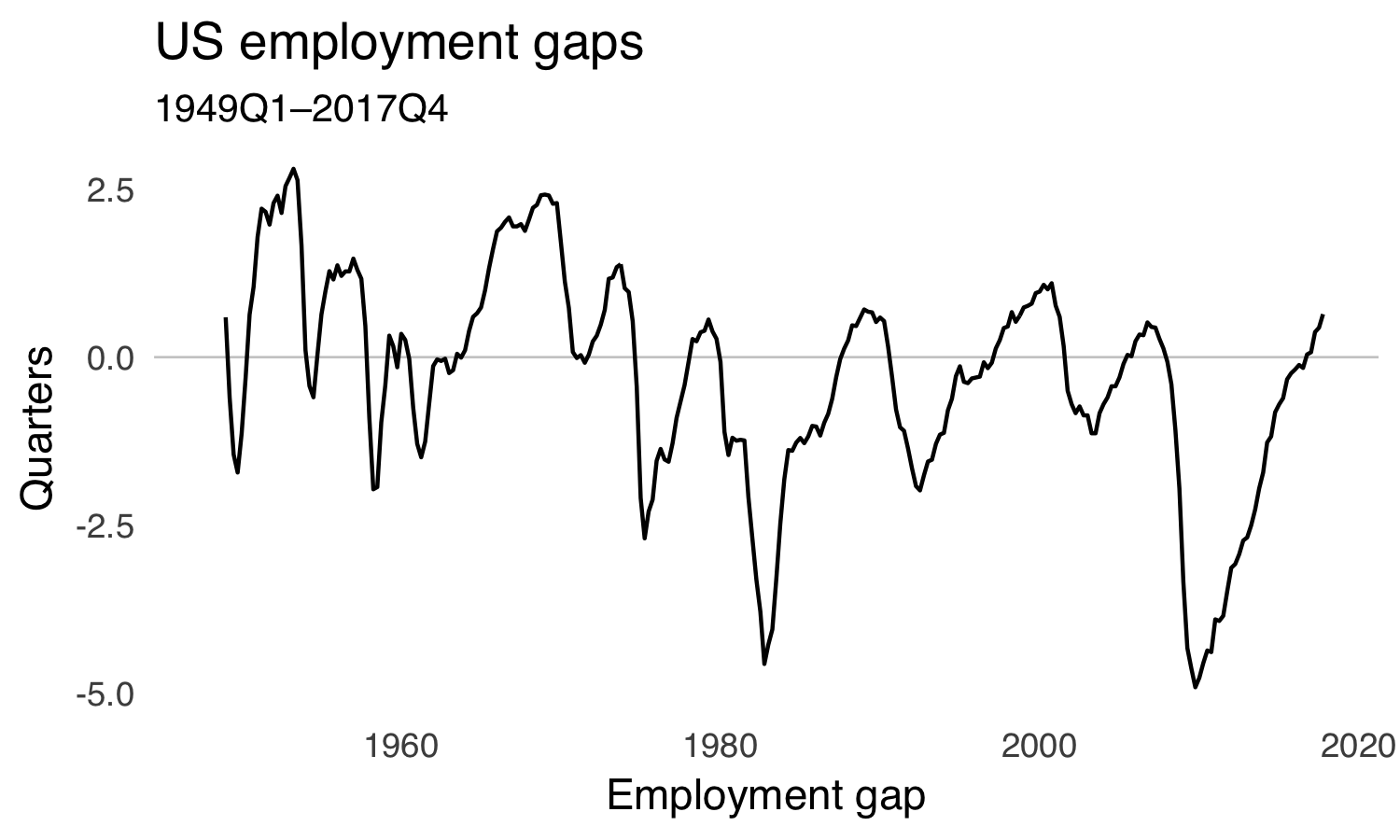

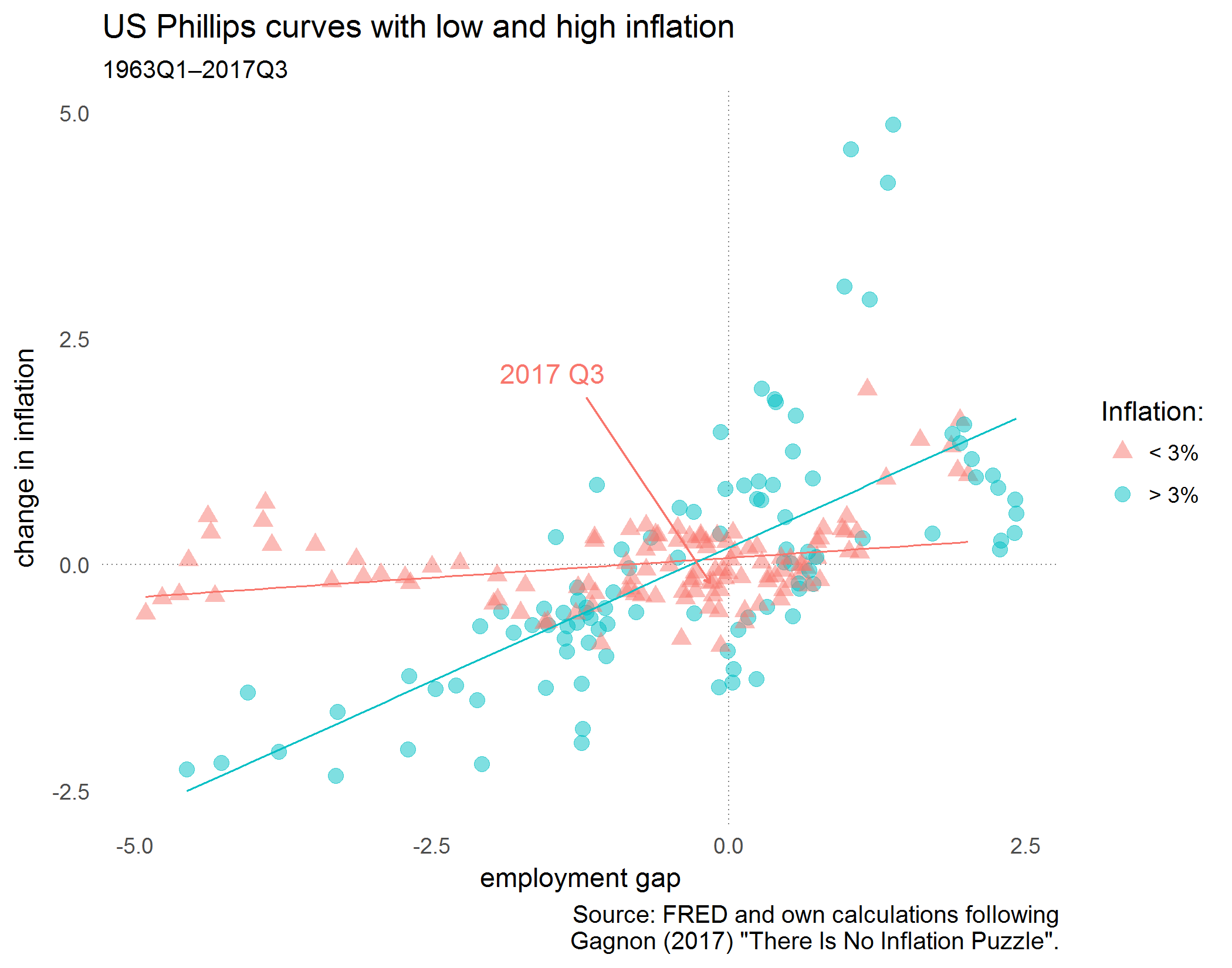

Joseph Gagnon has written a blog post at the Peterson Institute about the Phillips curve in the United States.

Some economists have observed that the employment gap turned positive this year, but inflation has not increased. Gagnon argues that we should not be too quick to infer from this that the Phillips curve relationship has broken down, as high employment may take a while to raise prices. And he adds that this relationship is weaker in low inflation environments due to hesitancies to lower prices (i.e., nominal rigidities).

He kindly provides data and codes at the bottom of his codes, but let’s try to reproduce his figure using only public data from FRED.

Download quarterly CBO estimates for the natural rate of unemployment from FRED and calculate the employment gap as current employment rate minus natural rate.

We see that the employment gap was negative for a long time after the financial crisis but has recently turned positive. That’s the bit of data that Gagnon and others are arguing about.

Now we create the variables that Gagnon uses. We lag the employment gap by four quarters and calculate the inflation rate as the year-on-year change in the price level:

Last, we check in which periods inflation (four quarters before) was above three percent. And we truncate the data to the same sample as in Gagnon’s analysis.

ggplot(df,aes(egap_l,cpi_change,color=high_inflation,shape=high_inflation))+geom_hline(yintercept=0,size=0.3,color="grey50",linetype="dotted")+geom_vline(xintercept=0,size=0.3,color="grey50",linetype="dotted")+geom_point(alpha=0.5,stroke=0,size=3)+theme_tufte(base_family="Helvetica",ticks=FALSE)+geom_smooth(method="lm",se=FALSE,size=0.4,show.legend=FALSE)+labs(title="US Phillips curves with low and high inflation",subtitle="1963Q1–2017Q3",caption="Source: FRED and own calculations following\nGagnon (2017) \"There Is No Inflation Puzzle\".",x="employment gap",y="change in inflation")+geom_text(data=subset(df,yq=="2017 Q3"),aes(egap_l,cpi_change,label=yq),vjust=-10,hjust=2,show.legend=FALSE)+geom_segment(aes(x=-1.2,xend=df$egap_l[df$yq=="2017 Q3"],y=1.85,yend=df$cpi_change[df$yq=="2017 Q3"]),arrow=arrow(length=unit(0.1,"cm")),show.legend=FALSE)+scale_colour_manual(name="Inflation:",labels=c("< 3%","> 3%"),values=c("#F8766D","#00BFC4"))+scale_shape_manual(name="Inflation:",labels=c("< 3%","> 3%"),values=c(17,19))

We see indeed that there’s a relationship, but it’s more pronounced in the high inflation regime. And the most recent datapoint “2017 Q3” shows that – a year ago – the employment gap was still slighty negative with -0.16 and the change in inflation in 2017 Q3 was also negative with -0.20.

I would generally characterize my state of mind for the last six to eight months as … poor. Not just because of current events in the United States, though the neverending barrage of bad news weighs heavily on my mind, and I continue to be profoundly disturbed by the erosion of core values […].

In times like these, I sometimes turn to video games for escapist entertainment. One game in particular caught my attention because of its unprecedented rise in player count over the last year.

[...]

I absolutely believe that huge numbers of people will still be playing some form of this game 20 years from now.

[...]

It’s hard to explain why Battlegrounds is so compelling, but let’s start with the loneliness. […] PUBG is, in its way, the scariest zombie movie I’ve ever seen, though it lacks a single zombie. It dispenses with the pretense of a story, so you can realize much sooner that the zombies, as terrible as they may be, are nowhere as dangerous to you as your fellow man.

[...]

Battle Royale is not the game mode we wanted, it’s not the game mode we needed, it’s the game mode we all deserve. And the best part is, when we’re done playing, we can turn it off.

In a recent paper (pdf), Ludwig Ensthaler, Olga Nottmeyer, Georg Weizsäcker and Christian Zankiewicz ask the following question:

Consider an asset that’s worth 10,000 euros. For 12 periods the value of either rises by 70% or falls by 60% with equal probability. Now consider these five buckets: 1) below 6,400, 2) 6,400-12,800, 3) 12,800-19,200, 4) 19,200-25,600 or 5) above 25,600.

The asset will be simulated for you and if you have guessed right and the asset ended up in your bucket, you get 20 euros. Else, you get nothing. Which bucket would you bet on?

My intuition would have been to go for the third bucket. But the right answer is the first bucket. The reason is that this question asks you what the most likely price for such an asset is, not for the average price. Ensthaler et al. offer the clue that one increase can’t compensate for one fall (0.4 · 1.7 = 0.68 < 1).

Let’s simulate this in R for many assets to see what this process is up to:

library(tidyverse)N<-5000# number of assetsT_per<-12# number of periods# Define matrix of asset pricesap<-matrix(NA,nrow=(T_per+1),ncol=N)ap[1,]<-rep(100,N)# initial asset price# Simulationfor(iin1:N){for(tin1:T_per){is_up<-runif(1,min=0,max=1)>0.5ap[1+t,i]<-ap[t,i]*(1.7*is_up+0.4*(1-is_up))}}

Next we extract some tidy statistics about our assets:

Now we can plot how prices develop over the 12 periods:

ggplot()+geom_line(data=stats,aes(x=period,y=value,color=series),size=0.8)+geom_hline(yintercept=100,size=0.5,color="black",linetype="dashed")+labs(x="Periods",y="Asset value",title=paste("Performance of",N,"assets after 12 periods"),subtitle="Price increases by 70% or falls by 60% with the same probability.",caption="See: Ensthaler et al. (2016).")+theme_minimal()ggsave("hidden-skewness.jpg",width=8,height=4)

Which produces:

All the assets start out at 100. The mean price of assets rises, but the median falls fast.

The authors conclude that people are bad at calculating compound interest rates and that we tend to neglect skewness.

References

Ensthaler, L., O. Nottmeyer, C. Zankiewicz and G. Weizsäcker (2016). “Hidden Skewness: On the Difficulty of Multiplicative Compounding under Random Shocks”. Management Science. doi